Know exactly what you're buying

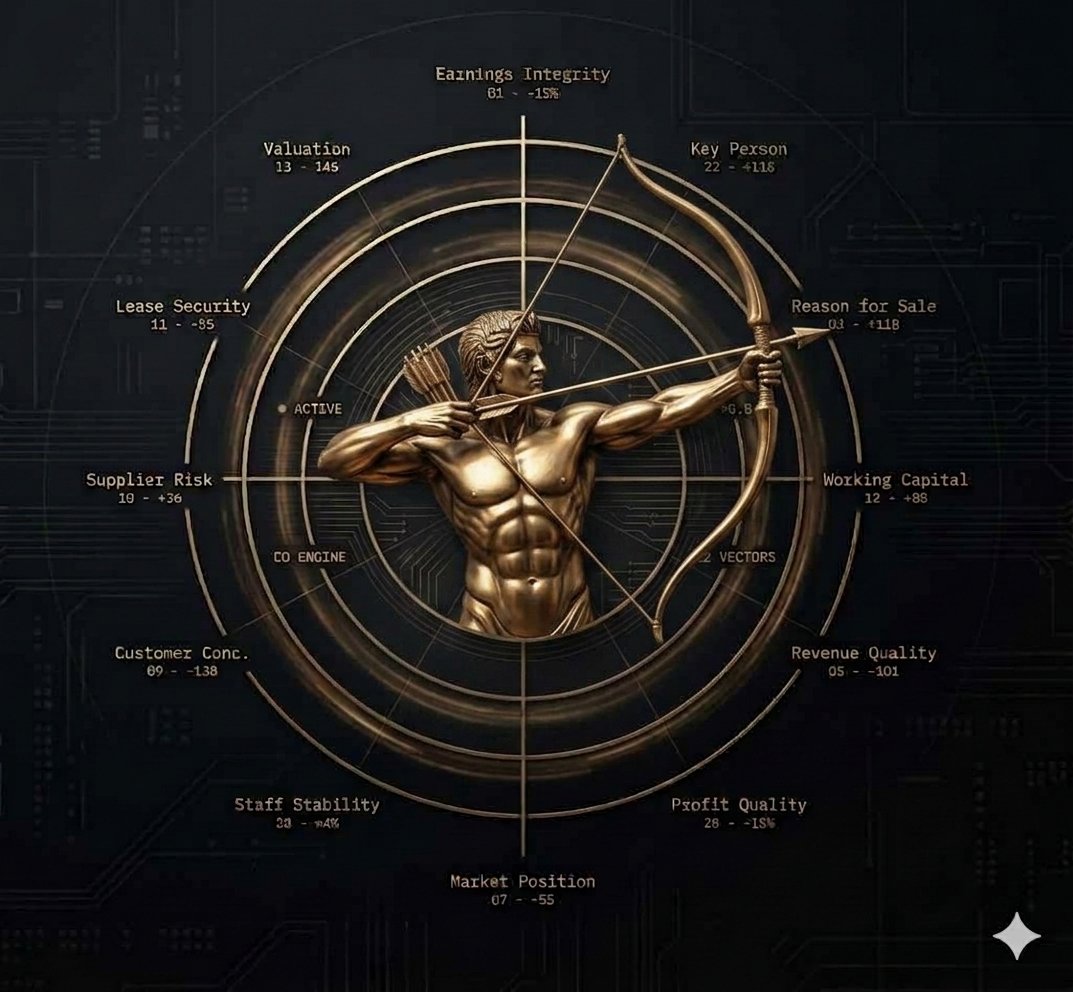

Five-page investor-grade analysis. QoE normalisation, three-year trend analysis, sector benchmarking, and a 12-vector risk matrix — then a verdict you can table with confidence.

A real deal. Fully rendered.

The complete Business Hunter intelligence report for Coastal Ridge Coffee Roasters — all six sections, every number, one page.

Issued 17 May 2026 · Valid 60 days

Prepared for M. Calloway / Calloway Holdings

HOLD — Do not LOI at ask. Reprice to £830K–£885K with wholesale earn-out.

Key risks: wholesale concentration (34%), EBITDA overstatement (£45K), lease expiry Aug-2027, roaster key-person dependency.

Coastal Ridge is a small-batch specialty roaster on a tourist-heavy coastal main street. Wholesale book of 23 active accounts, 1,840-subscriber DTC subscription, brand recognition that survives the seller. 4.8★ across 1,247 Google reviews. The product is real. The cash flow is real.

EBITDA add-backs are overstated by ~£45K. Wholesale concentration in two accounts (same hospitality group) with a handshake pricing deal — undocumented. Not deal-breakers. Deal-repricers.

⚠ Two restaurants in one hospitality group = £130,900 (34% of wholesale, 11.6% of total revenue). No signed supply contract since 2021.

34% of wholesale (11.6% total) in two accounts, one hospitality group. No written supply agreement since 2021.

→ LOI contingent on signed 24-month supply agreement. Earn-out: £75K at M18 if retained at ≥90% TTM.

Owner is sole certified Q-grader and roast profile architect.

→ 90-day full-time transition + 12-month part-time at £3.2K/mo. Fund Q-grader cert (~£6.3K).

No automatic renewal clause. Coastal main-street rents up 22% in 36 months.

→ Require seller to negotiate 5-year renewal with 3% annual cap before LOI is binding.

Add-backs do not survive operational-necessity test. True adj. EBITDA is £269,200.

→ Reprice. At 3.0× adj. EBITDA this is a £810K business, not £1.15M.

2019 Diedrich IR-12 (12kg) only production roaster. Operating at ~84% capacity.

→ Insurable. Budget ~£22K for backup 3kg roaster in year-1 capex.

Faster. Cheaper. More thorough.

| Business Hunter | Do It Yourself | Accounting Firm | Fiverr / Freelance | |

|---|---|---|---|---|

| Turnaround time | ✓Minutes | ✕Days to weeks | ✕4–8 weeks | •3–5 days |

| Quality of Earnings (QoE) | ✓Full waterfall | •If you know how | ✓Yes — at cost | ✕Rarely |

| Sector benchmark comparison | ✓Hardcoded, accurate | •If you have the data | ✓Yes | ✕Usually not |

| 3-year trend with charts | ✓Automatic | •Manual build | ✓Included | •Variable |

| 12-vector risk matrix | ✓Every report | •If you remember | ✓Included | ✕Rarely structured |

| Questions for the seller | ✓8 targeted Qs | •Your judgment | ✓Included | •Variable |

| Formal DD briefing note | ✓Included | ✕N/A | ✓They write it | ✕No |

| Cost | ✓Fraction of the deal | •Your weekend | ✕£8,000–£25,000 | •£300–£1,500 |

Business Hunter is not a substitute for legal or tax due diligence. It is the intelligence layer that comes first — so you only commission formal DD when the deal deserves it.

Have the listing pack? Drop it. 60-second read.

Drop a screenshot of the broker listing, P&L, or information memorandum. The Hunter will read every number in the image and give you an instant pre-analysis.

Pricing via Hunter Suite.

Business Hunter is part of the Hunter Suite acquisition intelligence platform. All plans are managed in one place.

Should you buy it?

Enter the numbers from the pack. Get a five-page investor-grade report in minutes — not weeks. Know before you commit.